Results

Higher profit, highest return

Bankinter once again ended 2017 with record profit, beating the figures achieved in 2016, even after taking into account the extraordinary items of that year. The Bank has shown itself to be more profitable than its competitors and confirmed its traditional competitive edge in asset quality.

Profit. Net profit amounted to 495.2 million euros (+1%) and pre-tax profit was 677.1 million euros, a similar figure to that of last year. Bankinter organically offset, with the customer business, 2016 profit, which included the extraordinary items recognised as a result of the acquisition of Barclays Portugal. In like-for-like terms, taking into account only the figures for the business in Spain, net profit increased by 20.2% and pre-tax profit by 19.1%.

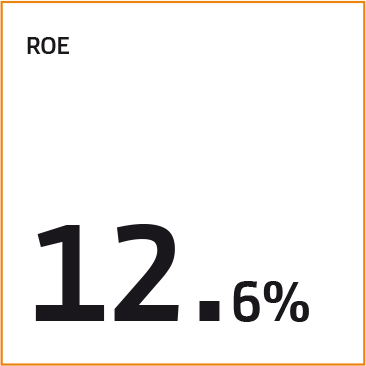

Return. Once again, Bankinter led the way in this item in 2017, with a return on equity (RoE) of 12.6%, the highest of Spain's listed banks.

Capital adequacy. The CET1 fully-loaded capital ratio ended the year at 11.46% and the CET1 phase-in ratio at 11.83%, six basis point more than in 2016 and well above the ECB requirement for Bankinter in 2018, which is 7.125%, the lowest in the Spanish banking sector. The liquidity gap was reduced by 200 million euros, standing at 5.2 billion euros at year-end 2017. The deposit-to-loan ratio reached 90.6%, 20 basis points higher than a year ago.

Non-performing loans. The NPL ratio fell to 3.45% down from 4.01% a year ago. If only the Spanish business is included, this ratio is even lower: 3.06%, less than half the sector average (8.08% in November). The foreclosed property asset portfolio was reduced significantly to 411.6 million euros (111.9 million less than in 2016), 44% of these assets were homes. The foreclosure coverage ratio stood at 45.2%.

Income statement margins grew strongly.

Net interest income. Increased by 8.5% to reach 1.062 billion euros.

Gross operating income. Amounted to 1.851 billion euros (+7.8%), thanks in large part to fees, the net amount of which increased by 11.7%, with the Asset Management business (+22.8%) particularly standing out.

Operating profit. This topped 900 million euros for the first time (906.8, million euros, up 11.3% on 2016). The 4.7% growth in operating costs (3% excluding Portugal) was offset by higher income, which led to an improvement in the cost-to-income ratio of the banking business, including depreciation and amortisation expense, fell from 48.6% to 46.8%.

Total assets on Bankinter’s balance sheet at 31 December amounted to 71.333 billion euros, 6.2% more than on the same date in 2016.

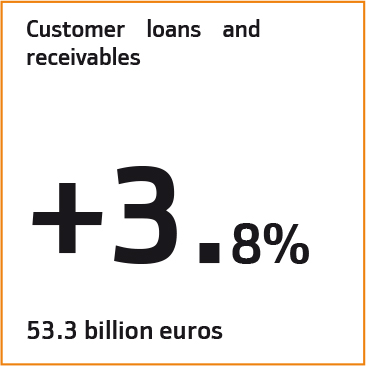

Customer loans and receivables. This reached 53.3 billion euros (+3.8%), despite total sector lending being reduced by 1.7%, according to the data for November.

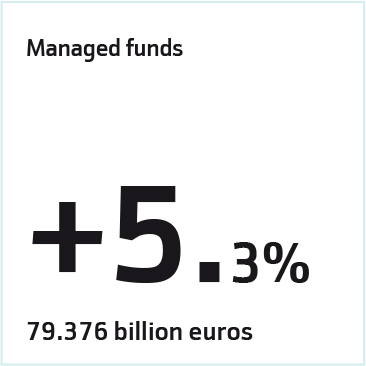

Managed funds. These amounted to 79.376 billion euros (+5.3%), of note among these were off-balance-sheet managed funds (investment funds, pension funds and wealth management) which increased by 12.9%.

The customer business was the main contributor to earnings. It is organised into five business lines, profitable and complementary to each other, which serve to diversify the Group's strategy .

Corporate banking. This area made the biggest contribution to the Bank's gross operating income, with 30%. The balance of the corporate loan book grew once again, reaching 22.9 billion euros (+5.2%). In the Spanish market it increased by 4.5% compared to the 3.4% fall recorded in the sector in November. The Bank has also attracted 18,600 new corporate banking customers in the year, 6% more than in 2016. Gross operating income from the international business was up 18.4% on the same period a year earlier.

Retail and commercial banking. Total private banking assets amounted to 35 billion euros at the end of December (+12%), with a growing proportion of it being in wealth management, which offers a better return. In personal banking, customer assets amounted to 21.2 billion euros, with 2.3 billion euros of net new assets obtained in the year. One of the star products in retail and commercial banking remains the 5% payroll account, which closed 2017 with a balance of 6.808 billion euros (+21.8%).

Línea Directa. Maintained the favourable trend of previous years, reaching a total of 2.79 million policies, with growth of 7.3% in car insurance and 13.5% in home insurance. Premiums increased by 8% to 797 million euros. The company had a RoE of 35% and a combined ratio of 86.9%.

Bankinter Consumer Finance. Now occupies one of the top positions in the consumer loan business in Spain and was one of the Bank's activites that grew the most in 2017. At the end of the year, it had 1.1 million customers (+28%) and loans of around 1.5 billion euros (+42%).

Bankinter Portugal. Improved under all the headings covered in its business plan, and in its first full financial year contributed 7% of Group income. Loans and receivables (4.8 billion euros) increased by 6%, with the performance of loans to companies being particularly impressive (+21%). Retail funds remained at the same level as last year (3.6 billion euros) and off-balance-sheet managed funds (investment and unit linked funds) rose by 25%. Gross operating income amounted to 133 million euros and pre-tax profit to 31.4 million euros.