Context analysis

Economic environment

2017 was characterised by synchronised global growth: the rate of growth gained inertia in the major developed economies, whilst the economic environment improved significantly in emerging countries, which had experienced more adverse economic conditions in the last few years.

In 2017, the eurozone confirmed its growth acceleration trend, which became more established and extended to a greater number of countries and productive sectors. Investment, consumption and exports were the main engines driving GDP growth in the eurozone above rates of +2.5%. European Central Bank (ECB) monetary policy continued to play a very important role, setting very low interest rates that are stimulating the demand for borrowing. This improvement in the economic cycle was evident in the labour market, where the unemployment rate fell to below 9%, compared to the high of 12.1% in 2013.

In 2017, the eurozone confirmed its growth acceleration trend, which became more established and extended to a greater number of countries and productive sectors. Investment, consumption and exports were the main engines driving GDP growth in the eurozone above rates of +2.5%. European Central Bank (ECB) monetary policy continued to play a very important role, setting very low interest rates that are stimulating the demand for borrowing. This improvement in the economic cycle was evident in the labour market, where the unemployment rate fell to below 9%, compared to the high of 12.1% in 2013.

Domestically, Spain once again stood out in a positive light, maintaining a growth rate of over +3% in 2017. The good performance of both domestic demand and exports, has led to more balanced growth, with the balance on current account remaining in surplus despite higher energy import prices. The labour market has evolved positively, with large increases in contributors to the Spanish social security system and a reduction in the unemployment rate down to 16.6%. Finally, the reduction in the public deficit remains on course, in compliance with EU fiscal consolidation targets.

The United Kingdom, on the other hand, has experienced a gradual economic slowdown. The uncertainty resulting from Brexit is acting as a brake on investment, while consumption has been hit by higher inflation due to the depreciation of sterling.

The US economy has shown fresh signs of its strength and has now grown for the last eight successive years. The dynamism of consumption continues to be the main factor driving economic growth, although both business and property investment have also performed positively. The continued high rate of job creation has also enabled the unemployment rate to be reduced to the 4% threshold. Finally, it is worth noting that the expected increase in disposable income and corporate profits resulting from the tax reform approved at the end of 2017 has generated a strong increase in confidence levels.

Japan is one of the countries that has performed surprisingly well in 2017, thanks to its return to growth. The Bank of Japan's expansionary monetary policy is beginning to bear fruit and the Japanese economy is awakening from a long period of very weak growth.

To end, we should highlight the improvement seen in the emerging economies. China has managed to put a brake on the slowdown in its economy and has maintained growth at levels around +7%, despite the persistence of certain imbalances, such as the high growth in lending. India recovered in the second half of 2017, after a first half which was somewhat disappointing; with growth losing impetus due to the difficulty experienced in adapting to certain structural reforms that will bring their rewards next year. Brazil came out of recession at the start of 2017 and the incipient growth has been accompanied by lower inflation, which has permitted looser monetary policy. Similarly, the general recovery in commodity prices is acting as a tailwind for other emerging economies like Russia and the countries of the Middle East.

Interest rates and foreign currencies

Interest rates have remained at low levels in the major economies, despite the Federal Reserve continuing to apply a strategy of gradual normalisation to its monetary policy. Inflation stayed at very moderate levels during 2017, in spite of the spike in commodity prices in the last part of the year. Structural factors such as demography, globalisation and technology have meant that inflation has not reached the targets of the central banks, who have adopted clearly accommodating policies.

Interest rates have remained at low levels in the major economies, despite the Federal Reserve continuing to apply a strategy of gradual normalisation to its monetary policy. Inflation stayed at very moderate levels during 2017, in spite of the spike in commodity prices in the last part of the year. Structural factors such as demography, globalisation and technology have meant that inflation has not reached the targets of the central banks, who have adopted clearly accommodating policies.

The ECB kept its rates unchanged in 2017. The benchmark interest rate remained at 0%, the deposit facility rate at 0.4% and the marginal lending facility rate at 0.25%. The ECB also continued to roll out its asset purchase programme for the amount of 80,000 million euros a month up to March and 60,000 million euros a month from April to December. The upturn in the eurozone cycle and forecasts of inflation closing in on its target of 2.0% in the medium term have led the ECB to announce a reduction in the asset purchase programme from 60,000 million euros a month to 30,000 million euros a month, from January 2018, an amount which will continue in force at least until September.

The Federal Reserve raised interest rates on three occasions in 2017, from 0.50%/0.75% to 1.25%/1.50%. The Fed also announced in September that it would start to reduce the size of its balance sheet and stop reinvesting some of the Treasury bonds and MBS that reach maturity. This strategy of gradual normalisation of monetary policy reflects the most advanced point that the US has found itself in during the current growth cycle; but it has not implied a hardening of financing conditions.

The Bank of England felt the need to raise its base rate from 0.25% to 0.50%, with the aim of slowing down the rising inflation triggered by the depreciation of sterling. Meanwhile, the Bank of Japan has persisted with its very loose monetary policy, characterised by a major programme of asset purchases and a benchmark interest rate of -0.1%.

The most notable factor in the foreign exchange market in 2017 was the strength of the euro against all other currencies. Of particular note was the appreciation against the dollar, from $1.05 to $1.20 over the course of the year, due to the following reasons: (i) The economic growth in the eurozone has been a positive surprise and has had more weight than the Fed's interest rate hikes which were already discounted by the market. (ii) The geopolitical risks facing Europe at the start of 2017 have taken on less importance because of the outcome of the elections in Holland, France and Germany. The euro has also remained strong against a pound, penalised by the uncertainty surrounding Brexit, and a yen, weakened by the extremely expansive monetary policy of the Bank of Japan and slower economic growth in the first part of the year.

Stock exchanges and bonds market

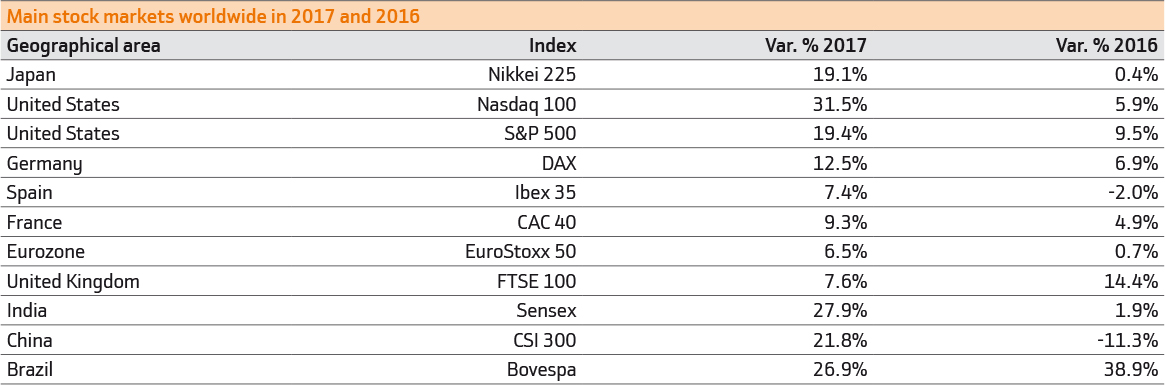

Stock exchanges performed well throughout 2017, with strong upside in the main markets. The improvement in the economic cycle, the growth of corporate profits and investors' search for higher returns than those offered by the fixed-income market were the main catalysts for equity markets. After a very good start to the year, European markets closed 2017 consolidating levels, without having recovered the highs reached in the first half of the year. The US, on the other hand, took the lead in the second half of the year and both the Dow Jones Industrials and the S&P500 achieved notable rises to reach record highs. The major spike in the shares of companies in the technology sector was one of the main factors driving this.

Stock exchanges performed well throughout 2017, with strong upside in the main markets. The improvement in the economic cycle, the growth of corporate profits and investors' search for higher returns than those offered by the fixed-income market were the main catalysts for equity markets. After a very good start to the year, European markets closed 2017 consolidating levels, without having recovered the highs reached in the first half of the year. The US, on the other hand, took the lead in the second half of the year and both the Dow Jones Industrials and the S&P500 achieved notable rises to reach record highs. The major spike in the shares of companies in the technology sector was one of the main factors driving this.

The gradual acceleration in domestic growth and the depreciation of the yen helped boost the Japanese stock market, while equities in emerging markets also performed well. The main emerging market indexes recovered strongly during the year, reflecting the improvement in the cycle in these countries and the gradual introduction of some structural reforms.

In the fixed-income market, the high volume of ECB purchases caused the German 10-year bond yield to be very reduced and below 0.50% for most of the year and peripheral countries' debt spreads to tighten. The process of fiscal consolidation carried out by these countries has also contributed to a reduction in risk premium. The ECB's expansionary monetary policy and the growing strength of company balance sheets has led to corporate debt spreads continuing to tighten. In the US, the debt market was characterised in 2017 by a gradual flattening of the interest rate curve. Despite short-term rates gradually reflecting the interest rate hikes implemented by the Fed, the rate on the 10-year Treasury bond remained at levels close to, but lower than, 2.50% for most of the year, which was one of very little volatility.

The table below shows, in local currency, the trend in the main stock markets worldwide in 2016 and 2017.