Credit risk

Credit risk is the possibility of incurring losses if debtors fail to meet their contractual obligations. Changes in credit risk are conditional on the economic and financial environment.

2017 was characterised by significant economic growth in Spain, despite ongoing financial deleveraging and stagnant lending across the financial system to households and non-financial entities with respect to the previous year, according to the Bank of Spain Statistical Bulletin. Within this scenario, Bankinter's trend towards moderate growth remained for another year. Lending to customers was up by 3.8% whilst computable risk (including off-balance-sheet risk) grew by 2.7%.

2017 was characterised by significant economic growth in Spain, despite ongoing financial deleveraging and stagnant lending across the financial system to households and non-financial entities with respect to the previous year, according to the Bank of Spain Statistical Bulletin. Within this scenario, Bankinter's trend towards moderate growth remained for another year. Lending to customers was up by 3.8% whilst computable risk (including off-balance-sheet risk) grew by 2.7%.

Non-performing loans

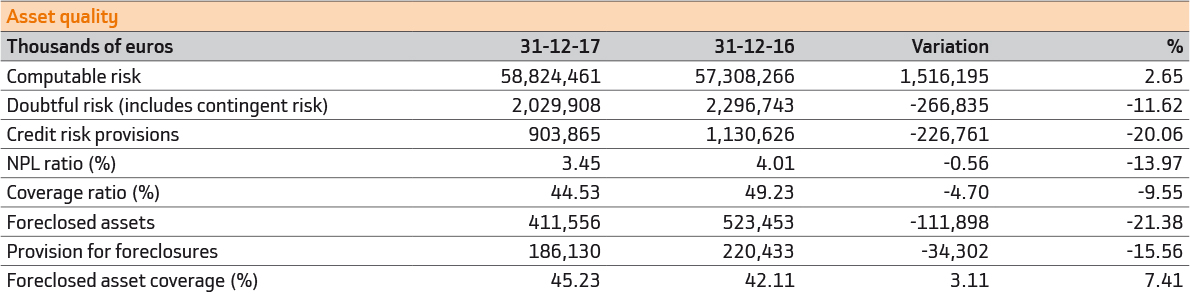

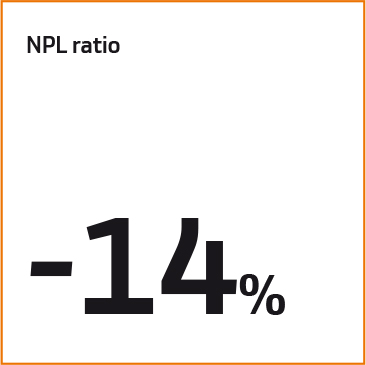

The non-performing loan ratio ended the year at 3.45%, a 56 basis-point or 14% decrease with respect to 2016. The non-performing loan ratio in Spain at year-end (3.06%) is 38% of the median for the industry (8.08% according to Bank of Spain data from November 2017). At year-end 2017, the foreclosed asset portfolio was 412 million euros, which was 0.7% of the total credit risk, a reduction of 21% in the financial year.

Evolution of NPL ratio (%) - Spain Evolution of doubtful assets and NPL ratio - Spain Evolution of the loan book

Distribution of the portfolio

Distribution of the portfolio

Over the years, Bankinter has tried to balance the distribution of its loan book between individuals and legal entities. Computable risk for individuals was 50.1% of the total, and that for legal entities was 49.9%. The most important characteristics are described below by segments:

Individuals. In 2017, the housing market and the financial situation of households continued to improve thanks to the good macroeconomic environment and, in particular, the trend in employment. Against this backdrop, lending to individuals grew by 1.0%, driven in particular by the growing momentum of consumer finance. The individual loan book amounted to 25.57 billion euros at year-end, with a non-performing loan ratio of 2.7%.

The residential mortgage loan book for individuals showed a loan-to-value (LTV) ratio of 61% at 2017 year-end and 87% of these loans are secured by the primary residence of the owners. The non-performing loan ratio of this portfolio was 2.5% at year-end. The average effort (measured as the proportion of income that the customer allocates to paying mortgage loan instalments) remained at very low levels (22%).

Corporate banking. The computable risk in corporate banking grew by 3.1% to 14,588 million euros, with a non-performing loans ratio of 1.2%. Bankinter pays close attention to this segment, the business activities of which are more international and less exposed to Spain's economic cycle and which has a solid competitive position based on specialisation, knowing the customer, flexibility and quality of service.

Small and medium enterprises. The small and medium enterprises segment recorded growth of 2.4%, its loan book stood at 11.127 billion euros with a non-performing loan ratio of 6.1%. The Bank applies automated decision-making models for managing this segment, along with teams of highly-experienced risk analysts.

Consumer finance. This business, operated through Bankinter Consumer Finance, had an excellent performance in the financial year, with growth of 38% up to 1.43 billion euros, 2.4% of credit risk. The risk-adjusted margin, and the non-performing loans ratios and costs, are controlled and are in line with the typical levels in this type of business.

Over the years, the Bank has tried to balance the distribution of its loan book between individuals and legal entities.

Developers. Bankinter maintains a very limited risk appetite in this segment, which enables the Bank to be very selective in its operations, which focus on first-class projects, in established areas, undertaken by solid development companies with a long history. Developer lending was 1.31 billion euros, representing 2.2% of the Bank's credit risk, which is well below the average exposure of the Spanish banking system.

Portugal. The Portuguese loan book contributed a risk of 5.274 billion euros to the balance sheet at year-end, with a non-performing loan ratio of 7.4%, and with provisions recognised for 79.7% of doubtful assets. In carrying out the business in Portugal, the Bank's usual high lending standards are applied.

Risk quantification models

Risk quantification models

Bankinter has used internal rating models as a tool for supporting its decisions regarding credit risk since the 90s. These models enable the Bank to assess the credit quality or solvency of transactions and customers and provide quantitative measurements of its credit risk. These models are mainly used to support approvals, set prices, quantify the coverage for impairment or provisions, monitor loan books, support recovery and facilitate active management of the loan books' risk profile.

The internal rating models provide homogeneous classes of solvency or internal ratings that group together customers/transactions with comparable credit risk. These models are also calibrated to assess expected and unexpected losses of capital. These metrics are fundamental for managing and monitoring credit risk at Bankinter.

The internal rating models provide homogeneous classes of solvency or internal ratings that group together customers/transactions with comparable credit risk.

Bankinter has rating models both for retail segments (mortgages, consumer spending, SMEs and so on) and wholesale segments, such as corporate banking. These statistical models are developed using customer, operational and macroeconomic information, combined in the wholesale segment with expert analysis. The models are updated and monitored on a regular basis to ensure their power of discrimination, stability and accuracy under a strict governance structure. The models committee and the executive risk committee are responsible for approving Bankinter's models. The risk committee also receives information on a regular basis on the status and monitoring of these models.

Exposure at default distribution according to internal categories