Bankinter achieved a net profit of 200.8 million euros in the first quarter, an increase of 8.7%, with solid growth in all its lines of business and all countries

Return on equity (RoE) consolidated at 17.4%, while RoTE was 18.4%. The efficiency ratio improved to 35.3% and the CET1 fully-loaded capital ratio increased to 12.5%, 466 basis points above the minimum required of Bankinter by the ECB..

The bank's balance sheet shows growth that outpaces the sector: lending (+5%), retail funds (+6%) and off-balance-sheet managed funds (investment and pension funds and wealth management/SICAVs) which grew by 18.2%..

Bankinter shows strength in all account margins: net interest income grew by 10.6%; gross income, which groups all revenues, by 6.9%; and operating income before provisions by 7.6%.

Bankinter Group began 2024 on the same growth path as in the previous year, with improvements in all balance sheet items and in all the businesses and geographical areas where the bank operates. Growth in volume – thanks to the consistency of its commercial strategy, effective management of spreads and momentum in the high-value customer segments – generated growth in all margins and consolidated the bank's position as sector leader in both efficiency and profitability. All of this has been achieved while maintaining a sound risk profile, with non-performing loans well under control.

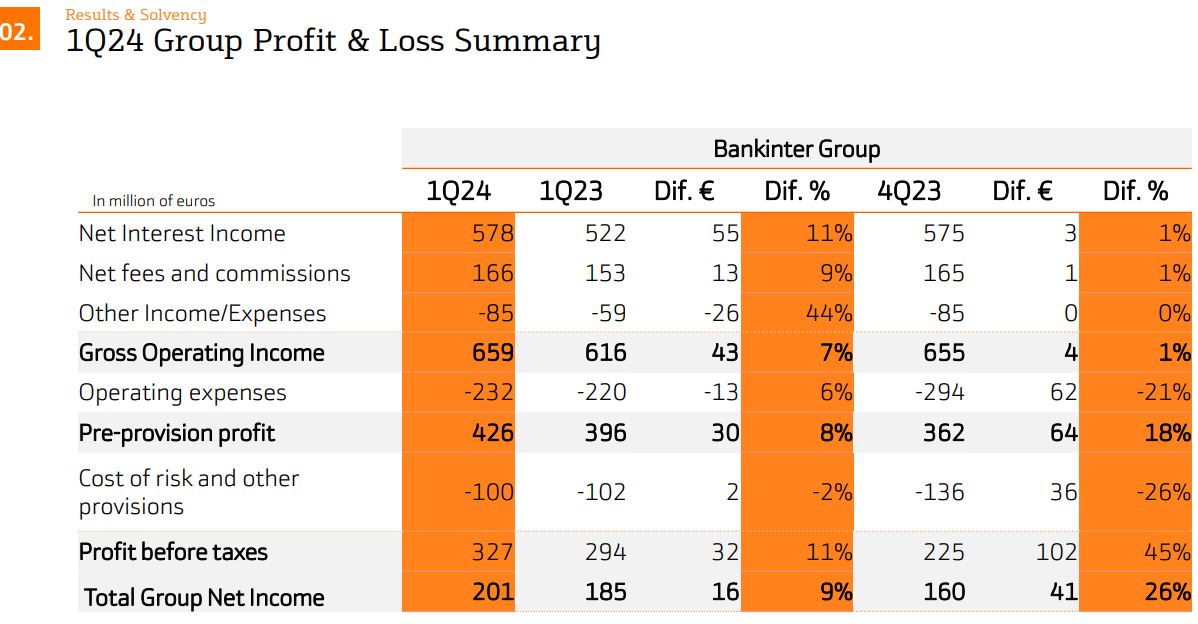

In the first quarter of 2024 Bankinter Group achieved a pre-tax profit of 326.7 million euros, 11% more than in the same period of the previous year. Net profit amounted to 200.8 million euros, 8.7% more than in the same period of the previous year. The impact for Bankinter of the new tax on the financial sector, fully accounted for in the first quarter, amounted to 95 million euros, compared to 77 million euros last year.

In terms of ratios, return on equity (RoE) consolidated at an excellent 17.4%, with RoTE at 18.4%, at the top of the sector in Spain.

The CET1 fully-loaded capital ratio was 12.5%, while the regulatory minimum the ECB requires of Bankinter is 7.8%, the lowest among listed banks in Spain, which implies a capital buffer of 4.66% (more than 1,800 million euros).

The NPL ratio remains at optimal levels: 2.2%, barely 5 basis points higher than a year ago. Spain's NPL ratio was 2.6%, up from 2.4% a year earlier, comparing very well with the sector average of 3.6% in January.

Of particular note was the efficiency ratio, which dropped to a successful 35.3% from 35.7% the previous year. This figure that is even better in Spain as a whole: 28.5%, leading the best figures in the sector.

Liquidity remains at optimal levels. The loan-to-deposit ratio is 103%, even higher than a year ago (102.6%).

Balance sheet figures.

The Group's total assets amounted to 112,938.3 million euros at 31 March 2024, 6.6% more than in the same period of 2023.

Loans to customers amounted to 77,041 million euros, 5.4% more than a year earlier. Spain's loan portfolio grew by 2.2%, a slightly lower percentage, given the weaker domestic real estate market, although the sector saw an average fall of 2.7% with data up to February from the Banco de España.

Customer retail funds amounted to 78,750 million euros, a growth of 6%, with strong growth in term deposits and a drop, albeit small, in account balances. The percentage growth in Spain was also similar and well above the sector average. Off-balance-sheet managed funds experienced notable growth, up 18.2% to reach 47,125.3 million euros.

Income statements.

All account margins showed significant growth compared to the same period of 2023, thanks not only to the still-positive trend in interest rates, but especially to the higher volumes of the loan portfolio and a commercial strategy that continues to produce good results in all the businesses and geographies where the bank operates.

Net interest income for the quarter amounted to 577.7 million euros, 10.6% higher than a year ago.

Gross operating income, which includes all the Group's revenues, increased 6.9% to 658.7 million euros.

Income from fees and commissions charged for the various services and value-added activities that the bank provides to its customers amounted to 213.3 million euros, up 4.7%, with 47.8 million euros coming from the Asset Management business, 17.6% more than a year earlier. Also of note was income from Collections and Payments, amounting to 45.6 million euros (+6.2%), and from Securities Trading, 40.4 million euros (+4.2%).

Net fees and commissions (difference between those collected and those that the bank pays to its partners in the Agent Network and Partner Banking) amounted to €165.8 million, up 8.5%.

Net operating income amounted to 426.4 million euros, up 7.6%, after incurring operating expenses of 232 million euros, 5.8% more than in the same period of the previous year. Of this, 128 million euros corresponded to personnel expenses, up 5%, and the rest to administrative and amortisation expenses. However, as revenues grew at a faster pace than expenses, the Group's efficiency ratio improved to 35.3%, 39 basis points less than a year ago.

Growing faster than the market in all businesses and geographies.

Bankinter has created a strategy of consistent long-term value that has enabled the bank to drive growth in all its lines of business, from the newest to the most consolidated, and in all the countries where the bank operates, each of which is beginning to play an increasingly important role in its contribution to the Group's income.

Within these countries, the greatest activity, business volume and revenue corresponds to Bankinter Spain, which, excluding EVO, closed the first quarter with a balance of 60,000 million euros in loans (+1.4% year-on-year growth), 67,000 million in customer funds (+5.4%) and 43,000 million in off-balance sheet funds under management (+20% year-on-year). Bankinter Spain's profit before tax amounted to 365 million euros, up 14% from the previous year.

The second most prominent geography is Portugal, where Bankinter experienced strong growth in all account items. On the balance sheet, the loan portfolio grew by 20% to 10,000 million euros; customer funds increased by 7.6% to 7,000 million; and off-balance sheet managed funds grew by a further 8% to 4,000 million euros. Bankinter Portugal's profit before tax amounted to 47 million euros, up 9% from the previous year.

In Ireland, loans amounted to 3,300 million euros, up 43% during the period, of which 2,400 million were mortgages, which grew by 53%. The NPL ratio of this subsidiary was only 0.34%. Profit before taxes amounted to 9 million euros in the quarter.

Looking at the various lines of business, Corporate Banking continued to make the biggest contribution to the bank's gross operating income, thanks to a specialised product and service offering, personalised to the customer's needs and very competitive. Building on these foundations, Corporate Banking continued to experience very positive growth. At the end of the quarter, lending to companies amounted to 32,900 million euros, 8.5% more than in the same period of 2023. Focusing on Spain, the growth of the corporate loan portfolio increased by 5%, compared to a drop in the sector of 3.7% with data up to February from the Banco de España. This means that Bankinter is continuing to gain market share in a shrinking market.

The driving force behind these good figures is International Business, which is playing a particularly important role in a context of growth in corporate export activity. The International Business investment portfolio at the end of the first quarter of this year amounted to 9,100 million euros, a growth of 15%. Some newer businesses, such as supply chain finance, have increased their volume fourfold during the period to reach 679 million euros.

As regards Commercial Retail Banking, the performance in the first three months was very satisfactory, particularly in terms of the volume of assets under management. In the Wealth Management segment, which groups together the customers with the largest assets, the bank managed a total of 65,500 million euros, 14% more than a year earlier. In this period alone, the bank attracted 700 million euros in new assets.

In the Retail Banking segment, assets under management grew 11% to 52,100 million euros, with net new assets of 600 million euros.

Noteworthy among the main products in the Commercial Retail Banking portfolio was the 18.2% growth in off-balance sheet managed funds. Among them, own mutual funds grew 14.9% to 13,960.1 million; funds of other managers marketed by the bank grew 18.2%, with a portfolio of 22,519.7 million; pension funds increased 14.5%; and finally, wealth management and SICAVs rose 29%.

The payroll accounts portfolio continues to establish itself as one of the bank's most important ways of attracting customers. The number of payroll accounts reached 547,000, 5% more than a year ago.

On the assets side, new mortgage production for the quarter amounted to 1,300 million euros, down 20% compared to the first quarter of the previous year. This is a consequence of various factors: the current weakness of the real estate and mortgage market, the seasonal factor of the Easter holiday falling in this quarter, unlike last year, and the comparatively lower figures for Bankinter Portugal, which had performed excellently in the first quarter of 2023 thanks to a powerful commercial campaign.

Notwithstanding all of the above, Bankinter Group residential mortgage portfolio grew by 2.5% compared to the same date in 2023, as the pace of repayments slowed. The bank also expects this market to pick up again in the second half of the year, in view of a possible fall in Euribor and a better-than-expected macroeconomic environment.

{kind=link}

{kind=link}

{kind=link}