Credit risk

Non-performing loans fall

while underperforming exposures grow

The economic activity and the effectiveness of public aid enabled non-performing and risky balances to remain at very low levels throughout the year. The outlook for the future will depend on the scale of the economic downturn and inflationary pressures. Households, companies and public administrations face a scenario of tightening of financial conditions, although the banking sector is in a much stronger position than in previous crises. Moreover, the normalisation of interest rates bodes well for higher returns in the sector.

Bankinter has been taking steps to shore up its balance sheet and management abilities to tackle adverse scenarios, particularly in terms of early warning and recovery systems. Note 46 of the Consolidated Legal Report provides much more details on this front.

Loans and advances to customers, expressed at amortised cost, increased by 8.3% and computable risk (including signature risks) increased by 8.9%, a remarkable and prudent growth in an increasingly uncertain environment.

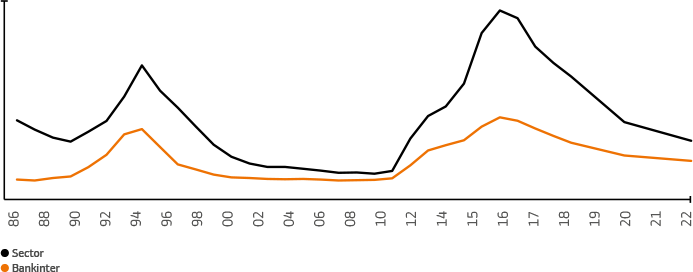

Underperforming exposures grew by 35.2%, mainly as a result of the reclassification of customers in the sectors most affected by the health and energy crises. Non-performing loans increased by 2.4% and the NPL ratio fell to 2.10%, a year-on-year reduction of 6%. The NPL ratio in Spain is 62% of the sector average (which is 3.77%, according to data from Banco de España published in October 2022).

Underperforming exposures grew by 35.2%, mainly as a result of the reclassification of customers in the sectors most affected by the health and energy crises. Non-performing loans increased by 2.4% and the NPL ratio fell to 2.10%, a year-on-year reduction of 6%. The NPL ratio in Spain is 62% of the sector average (which is 3.77%, according to data from Banco de España published in October 2022).

| Asset quality – Credit risk | ||||

|---|---|---|---|---|

| In thousands of euro | 31 December 2022 | 31 December 2021 | Change | Change % |

| Eligible exposures | 82,426,636 | 75,667,818 | 6,758,818 | 8.93% |

| Stage 1 (Performing loans) | 77,840,753 | 71,864,821 | 5,975,932 | 8.32% |

| Stage 2 (Underperforming exposures) | 2,851,278 | 2,109,457 | 741,821 | 35.17% |

| Stage 3 (Non-performing exposures) | 1,734,606 | 1,693,541 | 41,065 | 2.42% |

| Credit risk allowances and provisions | 1,150,700 | 1,076,381 | 74,319 | 6.90% |

| Stage 1 (Performing loans) | 175,134 | 203,711 | -28,576 | -14.03% |

| Stage 2 (Underperforming exposures) | 108,039 | 102,973 | 5,066 | 4.92% |

| Stage 3 (Non-performing exposures) | 867,527 | 769,698 | 97,829 | 12.71% |

| NPL ratio (%) | 2.10% | 2.24% | -0.13% | -5.97% |

| Non-performing loan coverage ratio (%) | 66.34% | 63.56% | 2.78% | 4.37% |

| Foreclosed assets | 122,865 | 170,655 | (47,790) | -28.00% |

| Provision for foreclosed assets | 68,813 | 89,767 | -20,954 | -23.34% |

| Foreclosure coverage (%) | 56.01% | 52.60% | 3.41% | 6.47% |

Changes in the NPL ratio (%) – Spain

Industry data source: Banco de España October 2022.

Following is a description of the trend and main figures for eligible exposures in Spain arranged by internal business sectors:

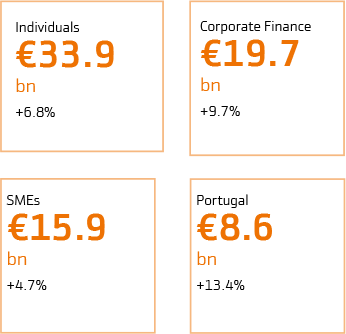

Individuals. In 2022, risk exposure to individuals in Spain grew by 6.8%. The portfolio at year-end stood at 33.897 billion euro, with an NPL ratio of 1.77%.

The residential mortgage portfolio of individuals recorded a loan-to-value ratio of 50%, with an 88% of these loans secured by first homes. The non-performing loan ratio was 1.4%. The average effort (measured as the proportion of income that the customer allocates to paying mortgage loan instalments) remained extremely low (23%).

Bankinter Consumer Finance contributed 2.832 billion in lendings in Spain, 26% more than the previous year, and closed the year with an NPL ratio of 7.2%. Risk adjusted margins, and NPLs and NPL ratios remained under control and in line with typical levels for this type of business.

Corporate Finance. Credit risk in Corporate Finance grew by 9.7% to 19,684 million euros an NPL ratio of 0.57%. In 2022 Bankinter prioritised growth in this segment, as it is more resilient to adverse economic circumstances.

Small- and medium-sized enterprises. The SME segment grew by 4.7% in 2022 and the portfolio stood at 15.881 billion euro, with an NPL ratio of 5.5%.

EVO Banco. EVO Banco, which focuses its banking business on individuals, contributed an additional 2.7 billion of credit risk to the Group in Spain (45% more than in the previous year), and an NPL ratio of 0.51%.

Portugal. Portugal's loan book represented a risk of 8.634 billion euro at the end of 2022, with a growth of 13.4% and an NPL ratio of 1.31%.

Ireland. The activity in Ireland, conducted through subsidiary Avant Money Plc (part of Bankinter Consumer Finance), brought to the Group 2.258 billion in credit risk at the end of the year. Of which 1.56 billion were home mortgages and the remaining 698 million came from consumer lending. Avant Money grew by 132%, with a NPL ratio of 0.40%. The emphasis on mortgage activity gives the business a very moderate risk profile.