Own funds

Many of the most developed economies in the world recovered their pre-pandemic growth levels in 2021, although Spain did not, despite the notable improvement in the economy.

With regard to the financial system, the European Banking Authority (EBA), in its December 2021 report, wrote about the existence of certain vulnerabilities linked to uncertainty over the credit granted within the framework of the support measures for Covid-19, the potential withdrawal of stimuli by central banks to curb inflationary pressures and a possible bubble in the value of certain assets.

In this context, the EBA, in collaboration with the European Central Bank (ECB) and the European Systemic Risk Board (ESRB), carried out its stress tests on the main entities in the banking sector in a hypothetical very adverse macroeconomic scenario. Bankinter achieved excellent results, which placed it as the strongest and most solvent Spanish bank and third among all the entities analysed.

To compensate for the potential effects of the COVID-19 pandemic on the financial system, and boost recovery, the ECB approved a series of regulatory changes to the regulations on the solvency of credit institutions, which included specific measures to positively contribute to capital ratios and to the provision of credit to the economy, such as support schemes for SMEs and infrastructure.

In addition, the European Central Bank (ECB) announced that banks may temporarily operate below the capital level defined as Pillar 2G (Pillar 2 Guidance) and the capital conservation buffer. These temporary measures were reinforced by the relaxation of the countercyclical capital buffer by the national macroprudential authorities. Similarly, it was stated that banks could partially meet the Pillar 2 (P2R) requirement with lower quality capital instruments, Additional Tier 1 (AT1) or Tier 2 (Tier2) capital.

Finally, and given the persistent uncertainty about the future economic impact of the pandemic, the ECB recommended that credit institutions exercise extreme caution when distributing cash dividends and paying variable remuneration to their employees.

All this, together with Bankinter's business model and its prudent risk and capital management policy, allowed the Group to operate with comfortable levels of high quality capital that are well above the requirements of the regulatory authorities and supervisors, despite the current economic context.

In 2021, Bankinter maintained the active management of its capital as one of its strategic priorities. The aim was to reinforce its position in terms of capital adequacy and to be able to face the economic effects of the pandemic, while preserving the flow of credit to the real economy with no major impact on its capital ratios. All the above, while considering the effects of the distribution in kind to shareholders of Bankinter's share premium, in the form of shares of the Group's insurance company, Línea Directa Aseguradora (LDA), and its subsequent listing on the stock market, which took place in April.

Recovery of the dividend policy

In addition, thanks to the good results of its evaluation by the supervisor and the EBA stress test exercise, Bankinter was able to resume its traditional policy of distributing dividends, resuming its payout level of 50% of the recurring earnings for the year, after the limitation on the distribution of dividends imposed at the start of the pandemic was lifted.

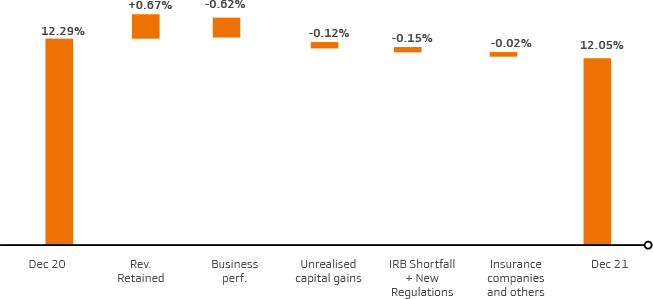

The highest quality capital of the Group, the CET1 ratio (ratio between ordinary Tier 1 capital and risk-weighted assets) stood at 12.05% at the end of 2021, 24 basis points below the ratio of the previous year. This was due to the high level of loans and receivables in the year, impacts due to regulatory changes in the definition of default, the estimation of the risk parameters of the loan book, the return to its usual policy of distributing cash dividends and the spin-off of LDA.

This level is well above the minimum ordinary capital requirement (CET1) established by the ECB for Bankinter Group in 2021 and which stood at 7.675% (the same as in 2020). The total capital ratio stood at 15.39%, also well above the total capital requirement established by the ECB for 2021 of 11.70%.

Variations in the CET1 ratio

The good results for the year, together with the impact of the spin-off of LDA, led to 67 basis points being retained in capital after the distribution of dividends.

The demand for credit throughout the year experienced strong growth both in terms of corporate exposure and in private mortgages. The introduction of support for SMEs and infrastructures brought about a flow of credit with decreased capital consumption. Other businesses also experienced growth in the year, with an increase in capital consumption due to market risk and operational risk. Changes in the business decreased the CET1 capital by 62 basis points.

The unrealised capital gains of the ALCO portfolio were gradually reduced by the evolution of the market and, although still positive, they caused a reduction of 12 basis points in the CET1.

Other effects impacted capital by 2 basis points.

In light of the improvement in market conditions in 2021, Bankinter issued 750 million euros of subordinated debt eligible as Tier 2 in mid-June 2021 to strengthen its capital base. The issue allowed the bank to supplement the capital levels that can be covered by this type of instrument and release higher quality capital (CET1) to improve its buffer, which is above regulatory requirements. In addition, this issue will make it possible to replace the Tier 2 subordinated debt of 500 million euros that was issued in 2017 and that has an early repayment clause from April 2022.

The MREL buffer

In December 2020, the bank received the communication of the Minimum Requirement for Eligible Liabilities (MREL) set by the Single Resolution Board for 2021. According to said communication, Bankinter would have to reach from 1 January 2022 (binding intermediate requirement) a buffer of instruments with a loss-absorbing capacity of 16.18% of the Group's consolidated risk-weighted assets and 5.28% of the exposure to the leverage ratio. Thanks to the generation of organic capital, balance sheet management and the issuance of 750 million euros of subordinated debt, the level of eligible instruments (e.g. MREL) stood at 21.69% as of 31 December last year (19.19% not including the capital required to cover the combined buffer requirement, which represents 2.5% of risk-weighted assets) and 8.13% of the exposure to the leverage ratio.

Outlook

For the 2022 financial year, the bank still seeks to generate organic capital growth so that it can operate with comfortable ratios higher than those established by the supervisor and to maintain its normal dividend policy, with 50% cash distribution of earnings. During 2022, despite uncertainties, the economic recovery of the geographies in which Bankinter Group operates is expected to continue. The bank's aim is to provide credit to the real economy so as to contribute to this recovery, with a return-risk trade-off that allows it to preserve its solvency, its profitability and its risk profile.