Credit risk

The economic recovery and the extension of public aid were decisive for the balances of unpaid and doubtful loans to remain at minimum levels throughout the year. How these develop in future will depend in particular on the effectiveness of the economic recovery and the rate at which the aid measures are withdrawn. The sectors most affected by the crisis -and the households whose jobs depend on them- remain highly vulnerable, because of the deterioration in their income and financial positions.

The significant increase in debt levels in public administrations makes the Spanish economy particularly vulnerable to any worsening in financing conditions.

Bankinter's risk management has been preparing for the vulnerabilities that could lead to deterioration of the loan book, although these have been less severe than was expected at the beginning of the crisis. The bank has adequate cover against such eventualities as a result of the extraordinary provisions made in 2020. Extensive additional information on this can be found in the "Impact of the health crisis" section of Note 46 to the Consolidated Legal Report.

NPL contained

In summary, for yet another year credit risk increased very moderately and with very contained NPL ratios thanks to the extraordinary measures taken against the pandemic and the bank's proactivity in applying them. Computable credit risk (which includes off-balance sheet risks) increased by 6.2% in the year.

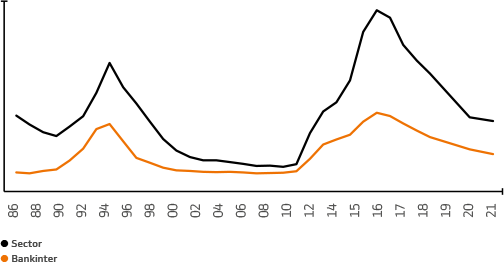

Underperforming loans increased by 29.8% due mostly to the reclassification of customers in the sectors affected most by the pandemic. Non-performing loans remained stable (+0.5%) and the NPL ratio fell to 2.24%, representing a reduction of 5.4% in the year. The non-performing loan ratio in Spain was 2.4% compared to the sector average of 4.29%, according to Banco de España data from November 2021.

| Asset quality - Credit risk | ||||

|---|---|---|---|---|

| Thousands of euros | 31/12/2021 | 31/12/2020 | Change | % change |

| Eligible exposures | 75,667,818 | 71,243,941 | 4,423,877 | 6.2% |

| Stage 1 (Performing loans) | 71,864,821 | 67,933,648 | 3,931,173 | 5.8% |

| Stage 2 (Underperforming exposures) | 2,109,457 | 1,625,086 | 484,371 | 29.8% |

| Stage 3 (Non-performing exposures) | 1,693,541 | 1,685,207 | 8,333 | 0.5% |

| Credit risk allowances and provisions | 1,076,381 | 1,020,270 | 56,111 | 5.5% |

| Stage 1 (Performing loans) | 203,711 | 212,511 | -8,801 | -4.1% |

| Stage 2 (Underperforming exposures) | 102,973 | 69,430 | 33,543 | 48.3% |

| Stage 3 (Non-performing exposures) | 769,698 | 738,329 | 31,369 | 4.2% |

| Non-performing loan ratio (%) | 2.24% | 2.37% | -0.13% | -5.4% |

| Non-performing loan coverage ratio (%) | 63.56% | 60.54% | 3.02% | 5.0% |

| Foreclosed assets | 170,655 | 227,145 | (56,490) | -24.9% |

| Provision for foreclosed assets | 89,767 | 110,241 | -20,474 | -18.6% |

| Foreclosure coverage (%) | 52.60% | 48.53% | 4.07% | 8.4% |

Provisions for credit risk increased by 5.5% in anticipation of the potential effects of the pandemic. This is fully explained in Note 46 to the consolidated legal report.

The balance of foreclosed asset decreased by 24.9% in the year to 171 million euros at 31 December 2021, equal to 0.3% of total credit risk.

Below is a description of the evolution and main figures by internal business units in terms of eligible exposures:

Changes in the NPL ratio (%) – Spain

Source: Banco de España, November 2021 for industry figure.

Source: Banco de España, November 2021 for industry figure.

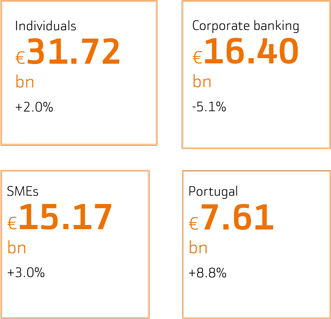

Individuals. Credit increased by 6.5%, with momentum in all segments. The individual lending portfolio totalled 31,724 million euros at year-end, with an NPL ratio of 2.0%. The home mortgage portfolio recorded a Loan To Value of 56% and 87% were secured by the borrower's first home. The non-performing loan ratio was 1.6%. The average effort (measured as the proportion of income that the customer allocates to paying mortgage loan instalments) remained extremely low (22%). Mortgage activity started up in Ireland the year before but took off last year, ending December with a balance of 424 million euros. Consumer credit returned to normal in the year and grew by 7.4%, with a business of 2.671 billion euros, 3.5% of the total credit risk. Risk-adjusted margins, and NPLs and NPL ratios remained under control and in line with typical levels for this type of business.

Corporate Banking. Credit risk in this area decreased by 5.1% to 16.403 billion euros with an NPL ratio of 0.66%. In this segment, where the business activities are more international and less exposed to Spain’s economic solid, Bankinter boasted a solid competitive position based on specialisation, KYC, flexibility and quality of service.

Small- and medium-sized enterprises. It grew by 3.0% in the year and the portfolio stood at 15,171 million euros, with a default rate of 5.2%. The Bank uses automated decision-making models to manage this segment, along with centralised teams of highly-experienced risk analysts.

Portugal. Its loan book contributed risk of 7.611 billion euros, with growth of 8.8% and an NPL ratio of 1.72%.