Basic principles of the risks function

Bankinter's exposure to risk is moderate, as demonstrated by the trend in the NPL rate, the conservative profile of the trading portfolio and the policy of neutralising the impact of interest rates on the balance sheet.

Bankinter carries on an activity with a prudent risk profile, seeking to have a clean and well balanced financial position and recurring profits so as to maximise the Bank's value in the long term.

Exposure to risks is deemed to be low or moderate, as shown by the comparative evolution of its non-performing loan rate, the reduced size and conservative profile of its trading portfolio, the general policy of hedging the impact of interest rates on the balance sheet and the active management of liquidity and operational risk and other potential risk.

The Bank also has rigorous corporate governance organisation and procedures. The Group has a solid risk culture, a highly qualified team of people and a set of advanced information systems which constitute basic pillars of the Bank's management.

The following is a summary of how risks evolved during the year. The principles, the governing and executive bodies and the management systems for risks in Bankinter are described in the Annual Report on Corporate Governance and in the document entitled Information of Prudential Relevance. Additional financial information can be found in the Group's Legal Annual Report. At the end of this section the location and the main sections of these documents relating to risk management are set out.

Credit risk

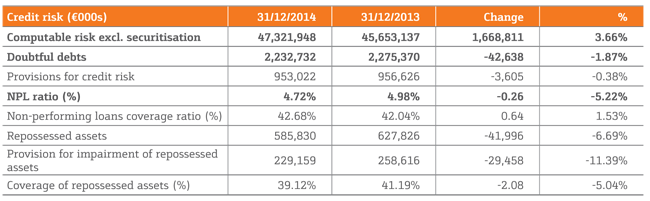

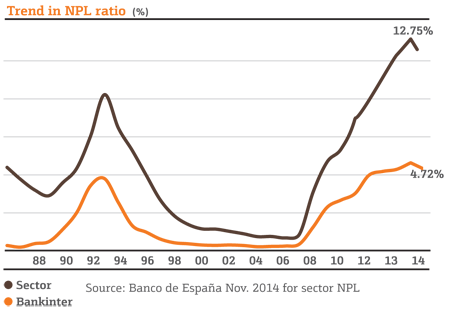

Bankinter ended the year with an NPL rate of 4.72%, 26 basis points less than the year before, increasing the favourable difference relative to the sector as a whole.

Economic environment and general trends

In 2014 in Spain the economic recovery that started in mid-2013 continued to consolidate. Forecasts of Banco de España in December 2014 for year-end pointed to GDP growth of 1.4%, basically underpinned by recovery in domestic demand (+2.2%) and with a reduction in the contributing of the export sector (-0.8%), and modest growth in employment (+0.8%) against

a background of falling prices (CPI -0.1%).

In accordance with the information from Banco de España, financing conditions in Spain continued to improve during the year except for isolated episodes of instability, and this allowed financing costs for businesses and households to be reduced. New lending increased, although total outstandings continued to fall: at the end of November, the balance of financing to non-financial businesses was still 4.8% below that of one year earlier, and that of financing to households was 3.9% down. The process of deleveraging thus continues, for businesses and households, although it has moderated and the financial cost of debt declined over the course of the year.

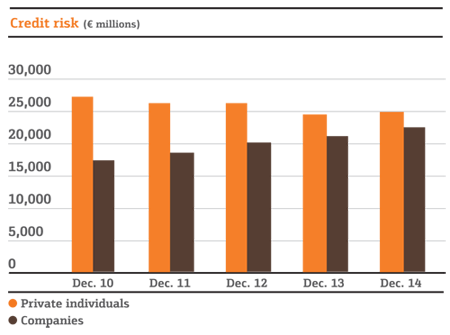

Bankinter has once again demonstrated its financial solidity in this context and has once again outperformed the sector as a whole. Thus the computable credit risk (which includes lending and contingent liabilities such as guarantees) grew by 3.7%. In 2014 lending to private individuals recovered, growing by 1.3% mainly as a result of the reactivation of residential mortgage lending, in which Bankinter is playing a leading role. Lending to companies grew by 6.4%, continuing the trend of recent years. At year-end, computable risk on private individuals represented 52.5% of the total, and that on companies 47.5%.

As for non-performing loans, the year ended with an NPL rate of 4.72%, 26 basis points less than the year before, 5.2% down. The favourable difference between this NPL ratio and that of the sector as a whole continued to increase, Bankinter's NPL rate at the end of the year being 37% of the sector average (which was 12.75% according to Banco de España data at November 2014). The volume of problematic and repossessed assets continues to be well below that of the Group’s main competitors. At the end of December 2014 the portfolio of repossessed (foreclosed) assets stood at €586 million, 1.2% of total credit risk, having been reduced by 6.7% in the year.

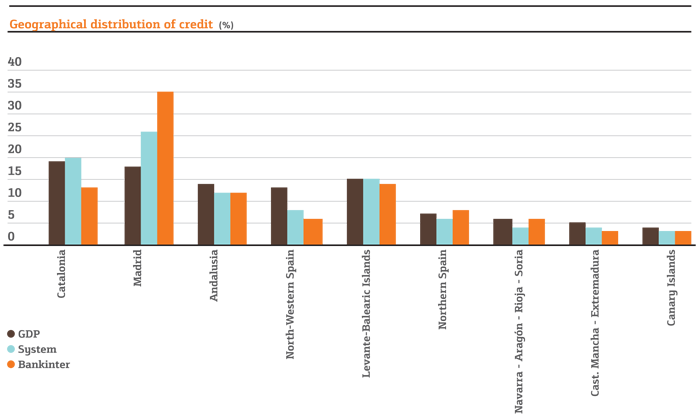

The Bank carries out regular monitoring of risk diversification by sector, geographical location, product, guarantee, customers and counterparties and has in place policies on maximum risk concentrations allowed. The following graph shows the geographical distribution of credit by regional directorates.

Private individuals

In 2014 there was gradual stabilisation in the real estate market, especially in the urban areas, in which Bankinter concentrates its activity. In this regard, the Bank has started selective residential mortgage lending campaigns within the parameters of high credit quality that characterise the Bank, which has led to net growth in lending to private individuals. The LTV (loan to value) ratio, which measures the ratio of the amount of the loan to the value of the property, was maintained at 59% at year-end, and 81% of the mortgage portfolio was secured by mortgages on residential property.

The private individuals portfolio maintains its high credit quality, amounting to €24,454 million at year-end, up by 1.4% (excluding lending to property developers) relative to the previous year.

Corporate Banking

Bankinter has many years of experience in this segment, the activity of which is more international and less exposed to the Spanish economic cycle and has a lower NPL rate. Lending to this segment stabilised in 2014, ending the year at 13,889 million, down by 0.3% on the year before.

Small and medium-sized enterprises

The economic recovery has allowed growth in lending to the small and medium-sized enterprise (SME) segment, risk on which amounted to €8,102 million at year-end, 19.9% up on the previous year. The Bank applies automated decision-making models to this segment, as well as having teams of experienced risk analysts.

Property developers

Bankinter applies extremely cautious criteria to the approval of property development transactions, as is shown by its low NPL ratio and its very limited exposure to this risk category, exclusively selecting viable projects of solid property developers that have performed well during the years of profound crisis in the sector for financing.

Loan outstandings on property developers at year-end were €875 million, which at just 1.8% of total lending continues to be well below the average exposure of the Spanish banking sector.

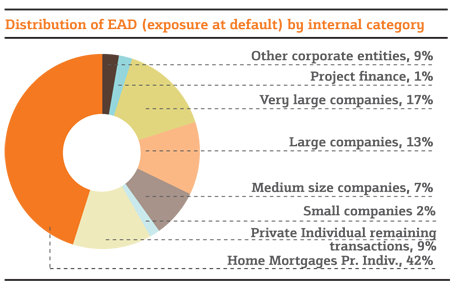

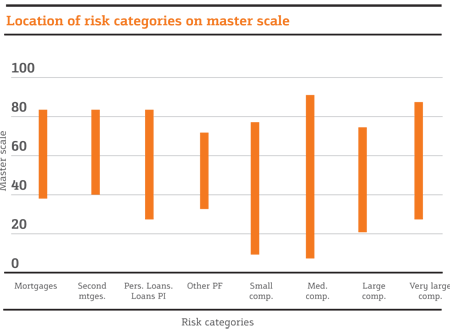

Risk rating models

Bankinter uses internal rating models as a supporting tool for credit risk decisions. These models enable comparative evaluations of the credit quality of transactions to be carried out, and provide quantitative risk measurement from approval on, facilitating the active management of the risk profile of the portfolios.

The internal rating models provide, for each category, a score or internal rating of the risk assumed by the Bank on each customer or transaction. Each of these ratings is associated with a certain probability of default (probability of a delay in payment longer than 90 days) and, accordingly, the higher the rating, the lower the probability of default.

In each risk category, whether relating to private individuals or companies, the range of probability of default associated with the rating of each one is different. In order to be able to compare the various credit risk categories, an internal master scale has been developed that gives a value in the scale to each default probability, where 0 is the highest probability of default and 100 the lowest. For example, the ‘home mortgage’ category is one with a relatively low probability of default and is therefore in the top part of the scale.

NPLs and repossessed assets

The year 2014 was characterised by stabilisation in the number and volume of new NPLs. In the last quarter of the year NPLs returning to the performing category (exits) started to exceed new NPLs (entries). The monthly average of the recovery ratio (exits/ entries) for the year was over 94%. Doubtful risk at year-end stood at €2,233 million, 1.9% less than at the previous year-end.

This reduction in doubtful debts, together with the increase in lending, enabled the bank to reduce the NPL ratio by 5.2% in the year, to 4.72% at the end of December. During the year, Bankinter continued to improve its recovery processes.

The portfolio of credit risk refinancing and restructuring transactions at the end of 2014 stood at €1,644 million, with any amendment to credit risk conditions being considered as refinancing. The majority of refinancing operations have additional guarantees.

The flow of non-performing loan balances was as follows:

Structural and market risks

Bankinter has limited exposure to interest rates and has covered its liquidity requirements without difficulty.

From the point of view of these risks, 2014 can be divided into two parts, with the second half of the year dominated by the sharp fall in oil prices, the accelerating depreciation of the euro and the increased volatility in equity markets. Other movements seen over the course of the year were the reduction in yield curves of peripheral euro zone countries, with the exception of Greece, whose yields increased substantially in the last part of the year due to political instability.

Structural interest rate risk

Bankinter has limited exposure to interest rate risk, neutralising the effects of changes in the balance sheet on the size of this risk. The situation of the interest rate risk map of the Bankinter Group as at the end of 2014 is shown in the graph.

Apart from this, dynamic simulation analyses are carried out. These tests enable us to estimate the sensitivity of the financial margin to various scenarios involving changes in interest rates. Similarly, but with a longer term view, the Bank analyses the effects that interest rate changes would have on its economic value.

The exposure of the financial margin to interest rate risk in the event of changes of +/- 100 bps parallel movements in market interest rates is +/- 3.6% for a 12-month horizon.

At 2014 year-end the sensitivity of economic value to parallel shifts of 200 basis points stood at 2% of equity.

Liquidity risk

Thanks to the ample availability of liquidity through the European Central Bank and the stability of customer deposits, this is not currently a critical matter in the financial markets.

Bankinter covered its liquidity requirements by using the liquidity facilities made available by the EBB and by turning to the international medium-term and long-term debt markets. During 2014 the Bank issued €400 million in mortgage-backed bonds under the EIB financing programme and €500 million of senior debt. The balance of commercial paper placed in the market traditionally considered as wholesale (counterparties in the financial markets) was €380 million as at 31 December. If major corporates are considered as wholesale, then the figure for commercial paper and commercial paper repos rises to €770 million on a consolidated basis.

We would also highlight the reduction, by more than €1.5 billion, in the liquidity gap, and the positive trend in the loans-to-deposits ratio, which stands at 78.3%.

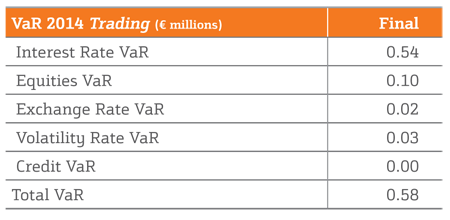

Market risk

In view of the instability seen in the past few years, Bankinter maintained the previous year's limits on VaR (value at risk). The following table shows VaR values of the trading positions at yearend 2014:

Apart from this, Bankinter also monitors the VaR of the portfolio positions of its subsidiary Línea Directa Aseguradora on a monthly basis, using the historical simulation method. The VaR of Línea Directa Aseguradora’s portfolio, based on the same assumptions, as at 31 December 2014, amounted to €2.04 million. Monitoring is also carried out of the possible risk that may be incurred by subsidiary Bankinter Luxembourg, applying the same method as that applied to the parent, VaR by historical simulation. In 2014 the estimated VaR was €0.04 million.

Operational risk

Through its participation in CERO (Consorcio Español de Riesgo Operacional, a private forum for financial institutions to exchange experience in managing operational risks) Bankinter ensures that it has access to best management practices in the sector.

Bankinter uses the Standard Method to manage its operational risk, in accordance with solvency rules in force. And through its membership of CERO (a private forum of financial entities for exchanging experiences in operational risk management), it ensures access to best practices in the sector.

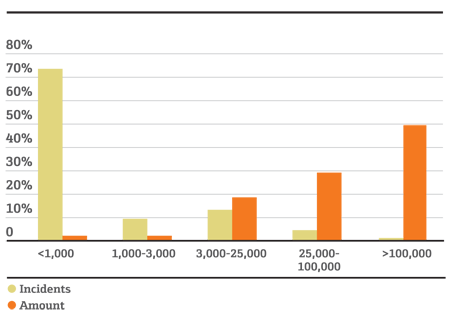

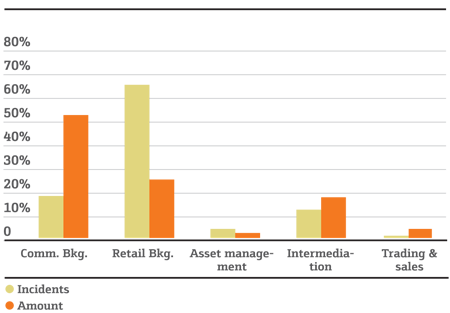

Operational losses are mainly (83%) concentrated in the branch network, even though most transactions are carried out through remote channels. This shows the significant role played by human error in operational losses and the strength of the automated systems and signup procedures of Bankinter's remote networks (Internet, Telephone Banking and sign-up by mobile phone).

As regards loss events, Bankinter's operational risk profile is shown in the following graphs:

Reputational risk

Reputational risk is defined as the risk associated with changes in perception on the part of stakeholder groups (customers, shareholders, employees, etc.) as a result of the brand's giving misleading information, failing to live up to expectations, lacking in transparency or breaking its promises. Reputational risk may arise from transactions of the company itself, from external events or from relations with third parties.

That is why it is so necessary to first measure and then monitor these risks and to develop scorecards for managing them.

The reputational risk map is crucial for identifying the risks and establishing degrees of prioritisation for them. The main risks and possible improvements to the risk management system are included in the corporate risk map. The corporate risk map is prepared by the Risks Function, under the supervision of the Chief Risk Officer and is presented annually to the Delegated Risks Committee of the Board of Directors.

One important aspect of anticipating reputational risk is understanding trends in the market and in the wider environment, as well as what is being said about the company in the media and social media. For this purpose Bankinter has a measurement system which analyses all this information and evaluates its reputational impact.

The Bank also has a system for periodically diagnosing and measuring the perceptions and expectations of its major stakeholder groups. This system, based on the RepTrak® methodology, enables the key reputational levers to be identified and action to be taken to influence the points of most concern.

The Bank's Product Committee identifies and evaluates any possible reputational risks before launching a new product or service.

Lastly, we should point out that the Bank's Corporate Reputation area takes care of the crisis management plan in order to establish the channels of communication and action protocols for any emergency or crisis, with a view to protecting the Bank's reputation and ensuring business continuity.

Additional information on the Group's risks can be found in the following documents and sections:

Legal Report

Contents

- Loans and receivables

- Non-current assets held for sale

- Contingent risks and commitments

- Risk policies and management

- Information required by Law 2/1981 on Regulation of the Mortgage Lending Market

- Exposure to the construction and property development sector

- Additional information on risks: refinancing and restructuring transactions. Sectoral risk concentration

Annual Report on Corporate Governance

Contents

- Scope of the Bank's risk management system

- Bodies responsible for preparing and executing the risk management system

- Main risks that might affect attainment of the business objectives

- Levels of risk tolerance

- Risks that materialised during the year

- Response and supervision plans for the Bank's main risks

Information of Prudential Relevance

Content

- Risk management strategies, objectives and policies

- Corporate governance of the risks function

- Structure and organisation of the risk management function

- Risk Appetite Framework

- Risk processes, methods, measurement and reporting systems

- Hedging and risk reduction policies

Download chapter in PDF

Download chapter in PDF