Summary of results

Bankinter achieved a pre-crisis level of results, with a net profit of €276 million, up by 45.3% on 2013.

The bank has doubled its profitability in just two years, achieving a ROE of 8.3%, one of the highest in the Spanish financial sector.

2014 was a turning point in the balance of problematic assets, being the first year to record a net reduction.

The most profitable and solvent bank. The Bankinter Group ended 2014 as one of the best capitalised and profitable institutions in the Spanish financial system, as demonstrated by the EBB stress tests, which placed Bankinter as the most solvent listed Spanish bank and one of the best in Europe, and as endorsed by the results achieved for the whole year.

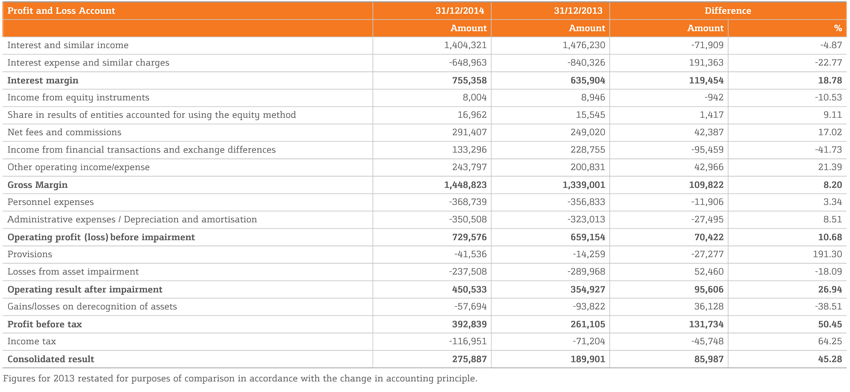

In 2014, the Group obtained a net profit of €275.9 million, and a pre-tax profit of €392.8 million. These are the Bank's best results in the last seven years, returning to pre-crisis levels in terms of both amount and recurrence.

Before carrying out the required comparison with 2013, it is important to note that, pursuant to the retroactive coming into effect of the new international accounting standard on levies (IFRIC 21), the ordinary and extraordinary contributions made to the Deposit Guarantee Fund in 2013 and 2014 have been recognised in advance. This involves restating the financial statements published for 2013 for purposes of comparison.

Taking into account this new standard, the Bank's net profit was up by 45.3% on the adjusted results for 2013 (€189.9 million as against the €215.4 million published at the time). Profit before tax for 2014 was 50.5% up on the readjusted figure for 2013 (€261.1 million as against the €297.6 million published at the time).

Without taking this standard into account, and comparing with the results for 2013 published at the time, the increase in the Bankinter Group's net income and profit before tax would be 28.1% and 32% respectively.

Irrespective of the basis of comparison, Bankinter obtained solid results in 2014, based on growth in income from typical customer business, which was up by 8.2% on the previous year, thus compensating for the fall in income from financial transactions.

A turning point in quality and solvency. 2014 was also a turning point in the balance of problematic assets, being the first year to record a net reduction. As a result, the Bank's NPL ratio in December stood at 4.72%, in comparison with 4.98% one year earlier. This figure is well below the sector average, which stood at 12.75% in November. At the same time, the sum of net additions to NPLs and bad debts continues to decline, with a consequent reduction in the allocation to provisions.

The good quality of the Bank's assets, at the highest level in the sector, is accompanied by reinforced solvency, capable of withstanding adverse scenarios as shown in the European stress tests. Bankinter ended the year with a CET 1 capital ratio of 11.87% in accordance with Basel III criteria. The figure would have reached 12.06% if the new accounting principle had not been retroactively applied. The fully loaded CET 1 capital ratio stood at 11.5% in December, one of the highest in the sector.

Similarly, it is important to note that Bankinter has a comfortable, balanced maturities structure, free of concentrations, with €1.2 billion maturing in 2015 and €1.4 billion in 2016. To meet them, the Bank has €6.1 billion in liquid assets, and the capacity to issue mortgage-backed bonds for up to €5.3 billion. As regards its financing structure, the Bank has succeeded in improving it, with a deposits to loan ratio of 78.3%, compared with 76.5% one year previously, and a funding gap down by €1.5 billion relative to year-end 2013.

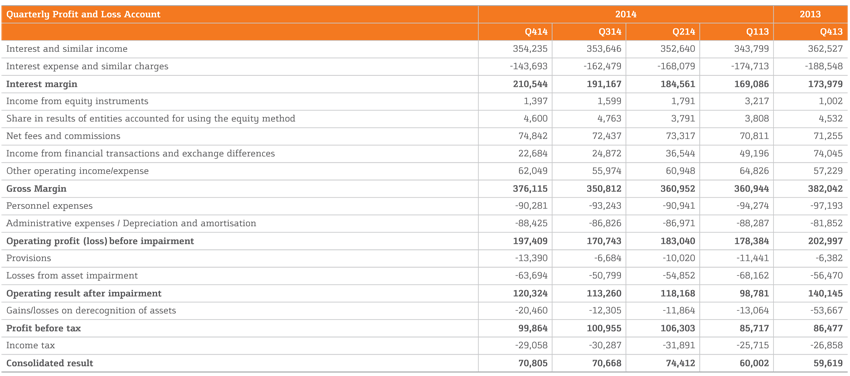

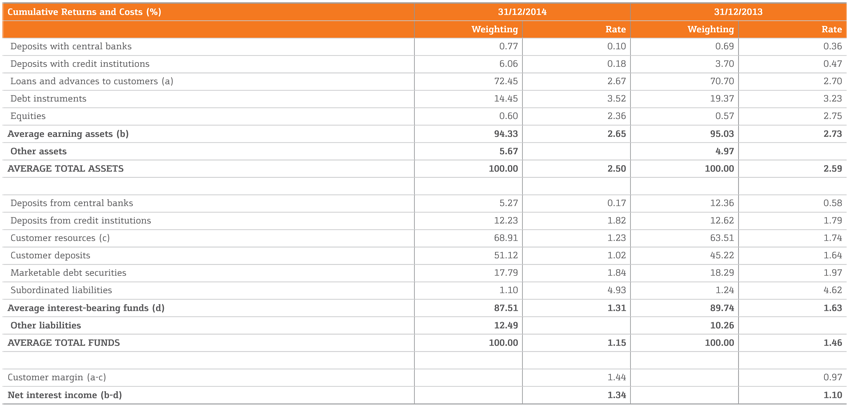

Growth in all margins. The positive results posted by the Bankinter Group for 2014 are based on typical banking business, not on returns from its fixed-income securities portfolio, and they show an improvement in all margins. The interest margin grew constantly throughout the year and also in comparison with previous years. For the year to 31 December 2014 it reached €755.4 million, up by 18.8% on the previous year. This sustained growth is based on the healthy evolution of the customer margin, which has improved over the year by 45 basis points as a result of the continued reduction of costs in resources.

The gross margin came to €1.45 billion, 8.2% up on the previous year, largely as a result of the satisfactory trend in fee income, which was up by 17% for the year thanks to increased customer business activity, especially in areas such as asset management and the equities business. Fee income compensated for the lower contribution from institutional financial transactions, where income was down by 41.7% on the figure for 2013.

The margin before provisions ended the year at €729.6 million, up by 10.7%, after absorbing an increase in expenses due to major investments made to support business growth, which did not however affect the cost-income ratio of the banking business, which improved in comparison with previous years.

As far as Bankinter's balance sheet is concerned, total assets grew from €55.16 billion at the close of 2013 to €57.33 billion this year, an increase of 3.9%.

As a result, Bankinter ended December 2014 with an ROE of 8.3%, as against 5.9% for 2013 and 4% for 2012.

Customer lending reached €42.45 billion at the end of 2014, up by 3% on the previous year. This positive development is due above all to another year of good progress in corporate business, with a lending portfolio up by 6.7% on the previous year, at €18.9 billion.

As of December, controlled resources stood at €55.45 billion, up by 8.7% on the previous year's figure. The increase in resources managed off-balance sheet was once again particularly significant (up by 40.7%); and within this, investment funds managed and marketed by Bankinter Asset Management, which increased by 39% to reach a volume of €11 billion.

As regards the quality of the Bank's assets, we would highlight the fact that 2014 marked a turning point in the trend in non-performing loans, with the balances both of NPLs and of repossessed assets falling for the first time since 2007. In this environment, Bankinter continues to have the best asset quality in the system. Thus doubtful debts ended 2014 at €2.23 billion, 1.9% less than in 2013, equal to 4.72% of the Bank's computable risk, which is 26 basis points less than it was one year previously.

The foreclosed real estate assets portfolio has been reduced after several years' growth in annual terms. At the close of 2014, its gross value was €585.8 million, 6.7% down on the previous year. It also had a cover of 39.1%. Furthermore, it is a very small portfolio in comparison with the other banks and is 44% concentrated in residential properties.

The Bank also increased the rate of sale of these assets by 14.5% in comparison with the previous year, proof of both the quality and good condition of the product offered and the Bank's sales capabilities in this business.

Improvement in all business lines. 2014 was very positive for all areas of customer business, which were confirmed as the driving force behind the Group's results. A key element of this was the healthy rate of new customer capture, with an increase of 24% in the number of new customers compared with 2013.

This growth in the customer base and higher customer business levels enabled the Bank to continue to strengthen the various headings on both the deposit and lending sides of its balance sheet. As far as customer lending is concerned, Bankinter was one of the few banks closing the year with an increase of 3% in overall lending, and 6.7% in lending to businesses.

As for the marketing of mortgage loans, for which the Bank has a highly competitive offering, we would highlight the fact that during 2014 the Bank tripled the volume of new mortgage lending posted in 2013, reaching €1.55 billion.

We should also point out that Bankinter granted seven out of every 100 mortgage loans signed in Spain in 2014, far in excess of the market share that could be expected in view of its relative size.

On the deposits side, Bankinter increased its retail funds (sight accounts, term deposits and promissory notes) by 7.2% over the year. With regard to the strategic businesses, special mention must be made of the healthy figures in Private Banking, in which Bankinter is now a fully consolidated player and a point of reference in the sector. Customer assets in this segment rose by 26% in 2014 in comparison with 2013, to reach €23.1 billion.

Over the year, the positive trends in other businesses have been notable, for example in the customer equities business, with a 23.4% increase in the number of orders executed and a 17.5% increase in the value of cash deposited in comparison with 2013. As a result, net fees from this business were up by 35.6% on 2013. There are two business lines that stand out as promising particularly strong performances in the coming years: consumer finance, which is already starting to post good results, and Personal Banking, which has been re-launched with new teams and products.

Download chapter in PDF

Download chapter in PDF