2015 was known for being a year of striking divergence in the pace of growth of different economies from a geographical perspective. Whereas the United States and Europe continue to fortify their respective paths to recovery, emerging economies face serious imbalances. Joined to the sluggish growth rates recorded by several of these and considerable deficits in their current accounts or their failure to make structural reforms, are external factors such as the fall in the price of raw materials, especially oil, the consequences monetary normalisation initiated by the American Federal Reserve has on their foreign debt, which especially affects those who have higher percentages of their debt in dollars, or the loss of momentum in China.

In 2015 the European path to recovery was still unremarakble. The newly found European economic recovery was backed by the European Central Bank (ECB), whose monetary policy was highly expansive. In its last meeting last year - December - it relaxed its monetary policy even more by cutting its deposit interest rate ( a further - 10 bp up to - 0.30%) and extended the period for its assets purchase programme, amongst other measures. Partly as a result of these activities, credit given in the Eurozone grew by +1.2% until November 2015, which strengthened the process of economic recovery.

In 2015 the European path to recovery was still unremarakble. The newly found European economic recovery was backed by the European Central Bank (ECB), whose monetary policy was highly expansive. In its last meeting last year - December - it relaxed its monetary policy even more by cutting its deposit interest rate ( a further - 10 bp up to - 0.30%) and extended the period for its assets purchase programme, amongst other measures. Partly as a result of these activities, credit given in the Eurozone grew by +1.2% until November 2015, which strengthened the process of economic recovery.

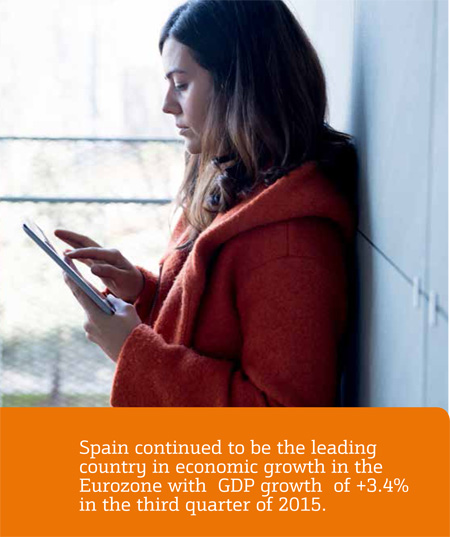

In the domestic arena, Spain, together with Ireland continued to lead economic growth in the Eurozone as its GDP grew by +3.5% in the fourth quarter of 2015. The improvement in the Spanish economy is supported by the recovery of domestic demand, driven in turn by household consumption and by the increase in business investment. There are already clear signs of an upturn in employment : In 2015 the unemployment figure fell by 354,200 and the number of people registered for Social Security rose by 533,186.

Amongst developed economies, the United States remained as the global leader, one year more, with year-onyear growth that was over 2% and showed a high amount of employment creation. The promising direction the American economy was taking allowed the Federal Reserve to begin the process of standardisation of its monetary policy at its meeting in December 2015, when it raised its reference interest rate by 25 bp, up to the 0.25%/0.50%.range.

Emerging economies continued to be the weakest link in the chain of global economic recovery. Two economies stand out for their poor performance: Brazil and China. Brazil, apart from experiencing a downturn in its economy in 2015 (- 4.5% in the 3T of 15) and a slowdown in the main economic sectors, faced high inflation (+10.7% in December 2015) and a strong depreciation of its currency. High prices compelled its central bank to keep raising its reference interest rate throughout 2015, up to low two-digit rates. The slowdown in the Chinese economy meant the global economy was subjected to considerable imbalance, not just due to the loss of momentum there, but because of the consequences this had on other economies.

All in all, the the global business cycle kept changing positively throughout 2015 at a slight, but expansive pace despite all the difficulties and vulnerabilities there were. In a sense, there was a comeback in the global economy last year, when the phase turned from downturn to growth.

A flexible monetary policy continued to be the dominant remedy among developed economies in 2015, despite the fact that the American Federal Reserve began standardisation of its reference interest rate in December. Everything seems to suggest that this process will be completed slowly and gradually throughout 2016 and always taking the most sensitive variables such as inflation or employment into account.

Inflation in developed countries remained at very low levels, and in some cases were even negative. These lower prices allowed the central banks of developed countries to keep their reference interest rates at historically low levels. Conversely, in some emerging economies, there was indeed some inflationary tension. This was true for Russia and Brazil, whose central banks saw the need to raise interest rates at various times last year. Using Brazil as a reference, at the end of 2015 the official interest rate there was no less than 14.25%, after having been raised five times. As for Russia, this rate was set at 11% at the end of the financial year.

Inflation in developed countries remained at very low levels, and in some cases were even negative. These lower prices allowed the central banks of developed countries to keep their reference interest rates at historically low levels. Conversely, in some emerging economies, there was indeed some inflationary tension. This was true for Russia and Brazil, whose central banks saw the need to raise interest rates at various times last year. Using Brazil as a reference, at the end of 2015 the official interest rate there was no less than 14.25%, after having been raised five times. As for Russia, this rate was set at 11% at the end of the financial year.

There were two matters of interest for the foreign exchange market in 2015: To and fro movements - appreciation and depreciation - of the eurodollar and drastic depreciation of the currencies linked to raw materials (ruble, Brazilian real, Canadian dollar, Australian dollar, etc.). Whereas it is possible to state that the eurodollar managed to level off in the 1.05/1.10 range throughout the year, the same cannot be said for the foreign currencies in a significant percentage of emerging markets. The yen tended to grow in strength, despite the aggressiveness of the monetary policy of the Central Bank of Japan, since at the most confusing market times, it behaved as a ‘ safe -haven asset’.

In short, it can be said that 2015 was a very different year for developed economies and emerging ones. Whereas the former ones kept reference rates of interest very low, despite the December interest rate rise in the United States, and had foreign currencies that were to a certain extent stable, the foreign currencies of the latter countries underwent depreciation and in some cases they were forced to raise their interest rates in an attempt to counter inflationary trends.

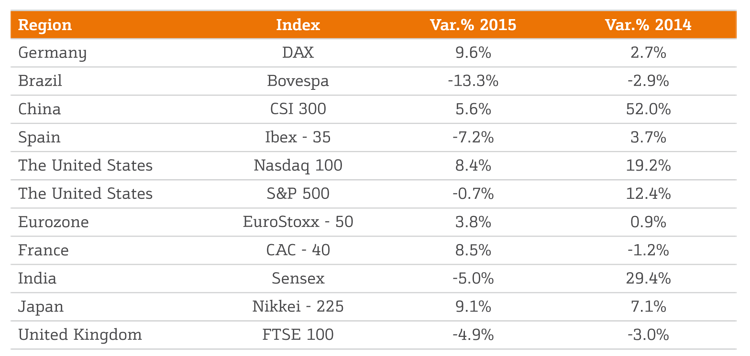

In 2015 there was a marked difference in profitability for the main indicators in developed economies. On the downside the Ibex-35 was noteworthy, falling by - 7.2% in the year, or the London FTSI 100 which fell by - 4.9%. However, other European stock markets offered acceptable returns, as did the EuroStoxx-50 (+3.8%) or the German DAX (+9.6%). It was a bittersweet year for the American market, since the S&P 500 closed with a slight fall (- 0.7%), whereas the Nasdaq climbed by +8.4%. The Japanese Nikkei yielded one of the best annual results among the stock exchanges of developed economies: +9.1%. It would be fair to say that 2015 was a year of contrasts, but not a bad year for the stock market.

As for the trends and market phases referred to, their annual change was marked by a very complicated summer, during which the main equity indicators were hit by slowdown in China, which in turn had a direct impact on the price of raw materials and particularly on oil. In 2015 the world economy was, at different times, affected by renewed misgivings over the solvency of Greece, the standardisation of the monetary policy of the American Federal Reserve, the unremarkable growth of business profits and the economic slowdown of emerging countries.

The bond market was propped up by the sharp drop in the price of crude oil, low rates of inflation and the bond purchase programme implemented by the ECB. Although in general bonds prices fell, these ended up being less than expected.

The following table shows how the main stock exchanges evolved over 2014 and 2015, always in local currency.