Private Banking had an excellent 2015. The first half of the year was positive, and subsequently slowed down due to customers' reservations as a result of the Chinese Crisis, as well as other issues that shook the market. From October, however, things went back to normal thanks to the Stock Market's recuperation, whose cycles largely depend on Bankinter's strategic activities.

The objective of Private Banking it is to increase its customrt base, in particular customers who are searching for a trustworthy portfolio manager in order to best optimise the profitability of their money, with reasonable security margins. Responding to these needs requires highly qualified staff who go through a process of continual training.

This trainings consists of staying up to date with knowledge, weekly meetings with Bankinter Asset Management leaders and a daily update on market developments. Thanks to this and to their independent judgment, private bankers offer the best advice with respect to investments and taxes, the two matters that concern customers the most.

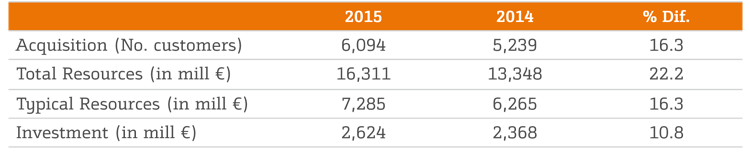

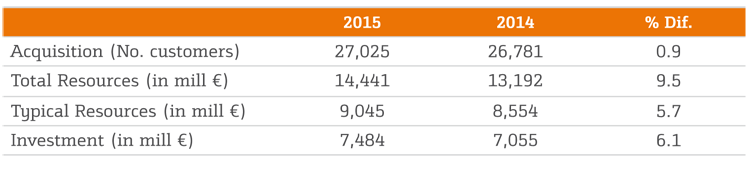

Reinforcements and improvements to the Private Banking service, as well as the constant renovation to its product portfolio, led to a new increase in net worth under management. The year ended with 28,000 million euros, 21% more than in 2014. In 2015, Bankinter also ranked second in a ranking for collective investment schemes (SICAVS), with 461 and an annual rise of 20%.

This means that one for every three SICAVS set up during the financial year corresponded with the Bank.

The reasons behind this success can be found in the rigorous selection process, good preparation and staff's sense of responsibility, which explains the increased quality perceived by customers. In fact, the Private Banking team is considered to be one of the best in the country. These achievements include the image of solvency and security that the brand transmits and the implication of Senior Management in achieving the objectives set out.

After three years of growth, the Private Banking division of Bankinter aspires to keep acquiring new customers in 2016, but also to earn their loyalty and to achieve a greater volume of delegated assets, either directly or via funds, maintaining the profitability achieved thus far.

The improvement in economic expectations, together with low interest rates, meant that in 2015 customers demanded new investment proposals. This provided business opportunities that had disappeared during the hardest years of the crisis and which reappeared during the recovery.

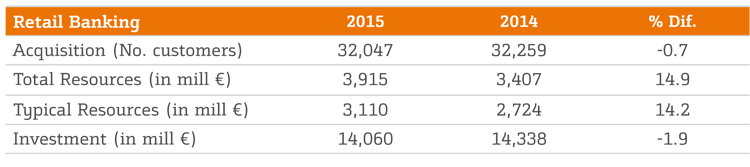

The switch in context coincided with the process of strengthening Personal Banking, the area of the organisation dedicated to the segment of customers with assets of between € 75,000 and one million euros. This customer group, requires custom-made management, specialised attention, a high level of service and a product offering which is adapted to the needs of each customer.

To reinforce this service, in 2014, Bankinter started a process to transform Personal Banking, as it had done previously with Private Banking (one of the hallmarks of Bankinter). To that end, the company embarked on a major effort to develop new products, improve customer service and the training of specialised managers to protect customers in this segment.

Personal Banking's activities operatate around a manager, with the aim of giving customers the best service possible. For this, the manager needs more and more sophisticated tools which allow him to properly develop his work. Thus, he is able to choose the financial products that best fit the customer's risk profile and needs, helping customers with a savings plan for their retirement, and providing solutions to their financing needs: mortgages, credit facilities, personal loans, etc.

The improvement and transformation effort paid off in 2015, with an increase of 6.4% in the number of active customers. The development of the ‘Non-Salary Account’, especially for the self-employed and entrepreneurs, and the ‘You and I’ Account, for couples with separate economies, contributed to the increase. The great challenge for Personal Banking is to consolidate changes that were put in motion throughout 2015.

In 2015, the market for private customers was characteristically highly competitive. Competition for the capture of customers was especially intense in two business areas:

• From the point of view of assets, the competitive pressure on mortgage lending increased. The result was a very significant decrease in the interest rate differentials offered and greater product diversification. Bankinter responded to the challenge of the market with innovative proposals, both fixed and variable mortgages. With a pioneering spirit, the bank also launched a mixed mortgage, which, for time intervals allows you to chose if the loan has a fixed or variable interest rate. The result of this strategy in the Individual customer segment was an increase in the contracting of new mortgages by 21%, which has meant the registration of 658.1 million euros worth of mortgages throughout the year.

The high level of activity during 2015 in the registration of personal loans in the Individual customer segment should be emphasised. During 2015, 134.7 million euros worth in registrations were taken, 46% more than in the previous year.

• From the point of view of liability, competition intensified especially in the Salary Account segment. Given the reduction in interest rates and the narrowing of margins, banks strengthened their proposals regarding acquisition related products. Bankinter was one of the first banks to offer very competitive returns on its Salary Account, where in certain conditions the client would obtain a high return on the money deposited. In 2015, the balance of the Salary Accounts portfolio increased by 22%.

In addition to these strategic lines of action, the company also developed other products to meet the needs of all customer profiles. This applies, for example, to the 'You and I' account aimed at couples who combine separate and common accounts, or to the Non-Salary Account in which the company proposed several advantages in return for linking receipts and spending per card. The offer of pre-authorised consumer loans, which are granted to selected customers who meet certain pre-conditions has also been strengthened.

Looking to the financial year 2016 no significant changes are expected in the personal market, so Bankinter will look into its strategies for customer acquisition, mortgages and salary accounts.

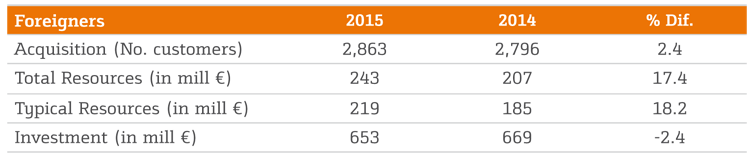

The market of individual foreign customers, centred most notably around mortgage financing, was consolidated in 2015. The number of new customers went up to 2,863, with an increase of 7% in active customers. Total resources also evolved in a similar way, with a rise of 17.4%. The amount from the contracting of new mortgages went up to 66.5 million euros, which meant an increase of 39% on the previous year.

The Foreign Client Segment is concentrated in coastal areas, most notably in the Mediterranean and in the Canary Islands, where they usually acquire a residence. For this, they need appropriate financing and they also demand high quality specialised services.

In order to provide this group of customers with the appropriate attention, Bankinter has highly trained staff with language skills and knowledge of their specific needs.

During 2015, Enterprise Banking had to become familiar with an environment characterised by the narrowing of margins, as a result of the fall in interest rates.

In order to grow, rationalise resources and improve its relationship with customrers, the bank completed a profound transformation in the area, the latter segmented the attention directed at companies into three levels, depending on their annual sales volume: SMEs (up to five million), Businesses (from five to 50 million) and Corporate (starting from 50 millions).

A new structure was created with the aim of growing and generating more income; of better managing customers by offering specific products, services and advice matched to the companies' needs according to their size; improving service quality; creating specialised centres for each segment; assigning specialised professionals in every segment and adapting Basel and European Central Bank criteria, which are going to be used to supervise the main Spanish and European financial institutions.

The transformation of the Business area required the reubicación of most of the customers, which today are allocated to new centres and mentors with a greater degree of specialisation.

The restructuring took place in phases. First, a pilot programme was completed in the Northern Area. Using the experience gained during the first half of 2015, the plan was extended to Madrid, Andalusia, the Balearic Islands and Levante. During the other half of the year it was the turn of the rest of the territorial network, which in Spain, at 31 December had:

Between the 22 corporate centres there are three dedicated exclusively to big corporations (customers invoicing more than 1,000 million): two in Madrid and one in Barcelona.

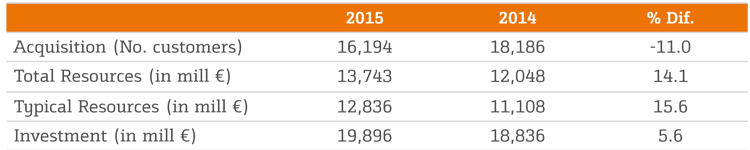

While proceeding with the restructuring, Enterprise Banking continued in 2015 with its ordinary activities, which resulted in a rise in investment to nearly 19,900 million euros, 1,100 million more, or 5.6% higher than at the end of previous year. Really significant was the growth in the volume of Signature Risk (documentary guarantees and business), which reached more than 2,900 million euros, after increasing by 21%. The market share of new business climbed to 5.4%, almost double that four years earlier.

Enterprise Banking earned a gross profit of 528 million euros, 1% more than in 2014.

Each of the three major segments of Enteprise Banking for 2016 is assigned specific objectives, always within the context of service improvement and results:

The Investment Banking service reinforced its leading position in the mid market in 2015, or segment of medium-sized companies. With a history of just four years, Bankinter Investment Banking has become the market's benchmark in this segment of financial activity.

Results from the area have benefitted from a global economic environment characterised by abundant liquidity and a low return on assets, which has resulted in a constant search for investment opportunities.

In this favorable context, the 2015 financial year confirms the growth expectations in the mid market segment, where the strength of the Bankinter brand and the relatively low level of competition provides the opportunity to reach wide areas of business.

Especially important, in this sense, is the reputation of the bank from the point of view of profitability and risk management (it has the highest return on equity and the lowest nonperforming loans rate in the sector), making it possible to overcome entry barriers and access a market with great potential for growth.

Bankinter's Investment Banking proposal is divided into four main areas. These concern its results and objectives:

Mergers and acquisitions. It is a market with a high growth rate, since it benefits especially from an abundance of liquidity and low interest rates. Cheap and accessible financing opens up more possibilities of leveraging this type of operations. In addition, narrow margins promote decision making and export consolidation, which also favours the expansion of the market for mergers and acquisitions. During 2015, Bankinter Investment Banking worked on 13 operations, giving financial advice to both industrial customers (23%) and financial customers (77%), having successfully completed the sale of Grupo Vitalia to Portobello Capital, among other operations.

Capital Market. A very strong first half of 2015 has allowed capital market operations as a whole (bonds and equities) to reach a record level in 2015. Bankinter participated in some of the most important ones, such as the floatations of Aena and Talgo, in addition to participating with special involvement in two capital enlargements carried out by Merlin Properties. Also deserving a special mention is our participation in a successful converible bond issue for IAG, just as in the high yield bond issues for other companies such as ENCE or Grupon Antolín. In order to respond to increasing demand (there are also good prospects for 2016), during the year Bankinter reinforced its broker, Bankinter Securities (formerly Mercavalor), with the addition of highly qualified teams to strengthen the analysis areas for companies and the distribution of fixed income and equities to domestic and foreign institutional investors.

An activity also in progress is that of private placements, these allow companies to finance themselves confidentially and are closely tailored to their needs by offering securities to a small group of institutional investors or even just one.

Structured financing. In 2015 a high growth rate was registered. It is an activity which entails more risk, but maintains levels of return higher than 3%, well above those offered by other assets. In 2015 operations were signed worth about 563 million euros and the portfolio rose to nearly 840 million. The objective for 2016 it is to maintain that level of growth.

Alternative financing. It solves the financing needs of companies which traditional banking service channels do not cover. Bankinter was pioneering when it entered this market in 2014, while limiting its scope to operations that generate value for companies. It is another niche activity with great prospects and, to enhance it, partnership agreements were signed with the Magnetar Capital find and the insurer Mutua Madrileña. In 2015, together with Magnetar, it signed a financing operation valued at 60 million euros. Similarly, Mutua Madrileña with Bankinter participated in the financing of an LBO (leveraged buy out operation).

The Investment Banking service's good results are based on a business strategy focused on supporting the company's network. Unlike the Anglo-Saxon model, where investment banking activities are usually segregated from commercial ones, Bankinter took the decision to create an interlaced structure.

In this way, the customer benefits at the same time from the proximity of their usual adviser and from specialised corporate advice. The model is also efficient for the company, since it generates a lot of long-term value for the network, strengthening the bank's brand and building client loyalty, although its development is more complex because it demands extra effort on the part of the commercial structure.

Therefore, the objective in the short and medium term is to enhance that strategy and make the best use of the advantages it offers.

During the period 2008-2014, the foreign sector served as a lifeline for Spanish companies, who took refuge in internationalisation to offset weak domestic demand. In 2015, the situation changed because of the recovery in home consumption and investment. However, the exporting base, that was expanded significantly during the crisis, has continued to be steady and has become part of the day to day activity of Spanish companies. In fact, companies no longer distinguish between business names (domestic or international) and require joint solutions to their needs.

Bankinter has adapted to these changes and it has made an all-inclusive commitment to support the consolidation of Spanish companies in foreign markets, starting from the idea that project knowhow is more significant than the meer financing of the same.

These are its main products:

Guarantees. The bank guarantees payment of the commitments and obligations that the company has acquired with third parties abroad.

Import letters of credit. It is a means of payment for importers in which Bankinter is an intermediary between the parties agrees to pay the exporter in the agreed form if the latter meets the requirements of the importer.

Export letters of credit. It is a means of payment by which a foreign bank, following its customer’s order, agrees to pay, accept or negotiate documents that will be presented through Bankinter, payable by one of its customers (payee).

Medium and long-term structured financing. Financial solutions for our customers which accompany the productive investment of Spanish companies abroad.

These financing operations of foreign activities are off balance exposures and have a low capital cost, which favours capital planning and compliance with the regulatory demands of the company.

Activity in International Business in 2015 was focused on the following lines:

Consolidatiion of strategic alliances with international banks, above all from France and Germany.

Participation in trade fairs both in Spain and in countries with a great potential for exports and investment in 2016, USA, Cuba, Southeast Asia, etc.

Intensification of training activities in the network to homogenise products and criteria.

The result of this effort has amounted to 48,000 million euros in brokered transactions, backed up by an investment of 2,700 million euros, having grown by 50% compared to 2014, which represents a 22% growth in net gross income in the international area.

The priority sectors were infrastructure, rail, renewable energy and the automotive sector; and the busiest regions were the Middle East, Europe, USA, Canada, Latin America and Africa.

For 2016, the goal is to maximise Bankinter's good credit quality and investment score, which allows it to offer better prices, especially in public procurement projects. Portugal's entry into the market also opens new lines of penetration.

Trading, distribution of treasury products and management of bank balances are incorporated into the Capitals Market.

Some of the main hallmarks of 2015 were consolidation of the improvement in the Spanish economy and stabilisation of the Treasury conditions for accessing financial markets. The European Central Bank's market interventions on monetary policy supported this stabilisation and also contributed to other eurozone issuers having better access to the market. Interest rates in the Eurozone have been lower due to growth and inflation being lower than foreseen.

Unlike with the Eurozone, the promising pace of the United States economy has allowed the Federal Reserve to create expectations of a rise in interest rates which in December led to the first change in these rates since the start of the crisis.

In the first part of the year the focus was on matters such as the Troika negotiations with Greece. And from summer, the situation of the emerging markets, especially China and Brazil, and the change in the price of oil created volatility and uncertainty in the markets.

In this setting, all Trading lines of business were active including the foreign exchange and, equity markets and particularly the fixed income market, with its status as a market creator for public debt and bills and co-leader in the issue of government bonds from the Spanish treasury.

The success of this organisation in the Private Banking and Personal Banking sectors, together with low interest rates have created great demand for the products designed in the Distribution area. Moreover, the excellent work of this organisation must be stressed in helping our customers access foreign exchange and fixed income markets and for the results obtained from their interaction with institutional customers.

As regards balance sheets management, the improvement in Bankinter´s liquidity position continued throughout the year backed up by the extraordinary gains in network resources and debt issues, positioning Bankinter as one of the most recurrent and respected issuers on international markets. In this regard, the great success of three issues of mortgaged bonds are noteworthy:

All issues were extensively oversubscribed. The diversification of maturity terms can be observed, which will minimise refinancing difficulties when they mature.

The bank's exposure to short term wholesale issues is still small and in December 2015, this figure stood at 547 million euros.

The institution's interest rate risk was monitored and managed, and it has remained at acceptable levels. Indeed, the positioning of the fixed income ALCO portfolio and balance sheet covers minimised the negative impact of Euribor interest rates, to which the majority of the bank's investments are benchmarked.

The bank's policy was to cover all structural foreign currency positions. In this regard, the Bankinter income statement was not affected by fluctuations in the main currencies in 2015.